05.11.26

GMA Insights | Top Q&A for SCoBA’s RFP for Low-carbon Cement

On April 8, 2026, the Sustainable Concrete Buyers Alliance (SCoBA), a program of GMA and RMI, launched its pilot procurement to accelerate the market for low-carbon cement. Since then, SCoBA has hosted a webinar targeted to suppliers (available to view here) and collected a number of questions about the RFP.

RFP questions and answers were published on April 27, grouped around common themes of ongoing and future engagement opportunities, applicability of the RFP to public procurement, registry development, RFP eligibility, and the content of RFP submissions. If you’re a supplier interested in participating in this RFP process, we invite you to take a look at the most frequently asked questions and answers below, and review the complete collection here. It is encouraging to see the strong engagement to date – there is clear enthusiasm to progress this market and we look forward to a robust set of RFP responses.

Top 3 Questions About the Sustainable Concrete Buyers Alliance Pilot RFP

- Will a registry rulebook be developed by SCoBA Organizers? How can the winning respondent expect to interact with the registry?

Ownership, tracking, and retirement of EACs will be managed consistent with the Book and Claim Framework and AIM Platform Standard and Guidance. Registries are considered best practice for long-term scalability and transparency of book and claim systems, and SCoBA intends to develop or partner with a centralized registry to support issuance, tracking, and retirement of EACs beginning in the second half of 2026.

If an interim tracking mechanism is used, contractual terms will recognize the interim mechanism to ensure EAC integrity and enforceability. For more on this, please see Section 2.3 of the Introductory Materials.

Internal supplier registries do not meet SCoBA’s registry requirements for this RFP. For this RFP, the selected Respondent(s) is/are required to work with SCoBA Organizers to ensure that the environmental attributes procured as a result of this RFP are registered appropriately at the time of cement EAC delivery and for subsequent retirement.

- Are supplementary cementitious materials (SCM) producers eligible to respond to this RFP?

SCoBA Organizers welcome SCM producers to respond to this RFP in partnership with a cement producer. As this procurement focuses on the cement functional unit, SCM technologies are eligible only when incorporated into a cement product that meets the RFP’s criteria including the emissions threshold. Section 2.1 of the Book and Claim Framework articulates the current approach to SCMs and describes a separate ongoing exploration into the potential for direct EAC issuance for SCM producers.

- How does physical delivery fit into the context of EAC delivery? How can physical offtakers get involved in SCoBA?

EACs are generated at the point of sale, after the physical cement product is produced and shipped, at which point the environmental attributes are decoupled and transferred separately to EAC purchasers. Physical offtakers receive the cement through conventional supply chains. To avoid risk of double counting, the physical product recipient is limited to qualitative claims as outlined in Section 2.5.4 of the Introductory Materials. For more information on physical claims, please review Section 8 of the Book and Claim Framework.

SCoBA procurements may incorporate a physical purchase opportunity where relevant and feasible.

The RFP is open until June 19! Companies with Scope 3 cement and concrete emissions who are interested in purchasing through this pilot procurement can explore SCoBA membership by emailing info@buildscoba.org.

Related News & Resources

05.07.26

GMA Insights | Harnessing Green Demand to Drive Sustainable Chemicals Production

Our latest GMA Insights installment is a co-authored article by GMA’s Andrew Alcorta and RMI’s Brianne Cangelose.

Chemicals play a critical, though often overlooked, role in modern society. They provide many of the key building blocks for the construction industry, support agriculture by increasing crop yields, and offer novel materials for a range of products from automobiles to new energy technologies. In fact, chemicals are everywhere, present in 96% of manufactured goods, including 75% of the energy technologies that will be needed to navigate the energy transition.

While chemicals are deeply embedded in modern society, it is equally important to acknowledge the challenges they pose. Among these are the need to reduce reliance on fossil inputs, develop better end-of-life management for chemical products, and lower emissions even as production is projected to grow up to 43% by 2050. More effort is needed across all these fronts, but addressing the 2 billion metric tons — or roughly 5% of global greenhouse gas emissions — from chemical production annually requires particularly urgent action given the long timelines to commercialize new production methods.

Despite these challenges, technologies are emerging to enable low-emissions chemicals production. While many of these technologies show technical promise, few have moved beyond the pilot or early demonstration phase. Scale-up of these technologies is often not held back by technical feasibility so much as by commercial barriers, including uncertainty about demand for low-emissions products and risk-aversion among participants spread across long and complex chemicals value chains.

Clear demand signals from companies that use chemicals in their products and novel mechanisms to bridge chemicals value chains are critical to overcoming these roadblocks and unlocking investment. The Center for Green Market Activation (GMA) and RMI are actively working to establish demand signals by aggregating buyers of low-emissions chemicals and by developing a book and claim system to enable chemical producers to transact directly with downstream companies that have committed to lowering supply chain emissions and are willing to pay a premium to do so.

The Challenge of Decarbonizing Chemicals Production

Scaling low-emission technologies in the chemicals sector is uniquely challenging. Chemical production assets are highly capital-intensive, with investment horizons that span decades. Existing plants, many of which are fully depreciated and can produce at a low marginal cost, leverage processes that have been optimized over many years and produce at enormous scale. The result is constant cost pressure that reinforces the competitiveness of conventional production methods. As a result, even when low-emission alternatives exist, buyers and suppliers alike often default to the legacy status quo.

The diversity of chemical products — and the resulting complexity of value chains required to produce them — results in an additional challenge. Unlike other industries with relatively standardized products, the chemical sector encompasses thousands of molecules, intermediates, and derivatives. This often results in long value chains with multiple layers of intermediaries separating a primary chemicals producer, generally responsible for the majority of emissions, from the better-known companies at the end of the value chain that have made net-zero commitments and are closer to consumer demand. In the middle are specialized producers of intermediate chemicals or products that often operate with thin margins and limited visibility.

In this environment, intermediate producers operating with thin margins have few incentives to source lower-emissions, higher-cost inputs unless they have certainty that their customers are willing to pay an equivalent price premium. The result is an enormous coordination challenge. Multiple parties within a value chain must simultaneously close both procurement and offtake contracts at a material premium to market prices. And all of this needs to occur at a volume that gives the primary chemical producers certainty that customers will pay a premium for most of their output over an extended time horizon. While this may be possible in rare cases where large buyers directly purchase from primary chemical producers, it will be all but impossible in most chemical value chains.

Leveraging Novel Mechanisms to Catalyze Investment

Breaking the deadlock requires both credible demand for low-emissions chemical products and mechanisms to bridge companies across long, complex value chains. GMA and RMI believe that two critical interventions, pursued in tandem, have the potential to address these challenges and unlock investment in low-emissions chemical production: demand aggregation and book and claim.

Demand aggregation is the first necessary intervention. As in many industrial sectors, low-emissions production will come at a price premium, particularly given that novel technologies often operate at small scale and with less historical process optimization than their fossil-intensive counterparts. While new technologies have the potential to decrease costs as they scale, the ability to achieve initial traction in highly price-sensitive markets is often a challenge for these production methods. The presence of buyers willing to purchase at a premium is a critical proof point for projects seeking capital to invest in low-emissions production.

But why is it necessary for multiple buyers to act together in order to provide this proof point? Because chemical assets operate at such a significant scale and because their lifetimes are so long, the purchasing volume required to unlock investment in a new facility can be enormous. By pooling demand, multiple buyers can provide the necessary volume to support an investment decision, thereby decreasing the cost and risk that any individual company would otherwise have to take on.

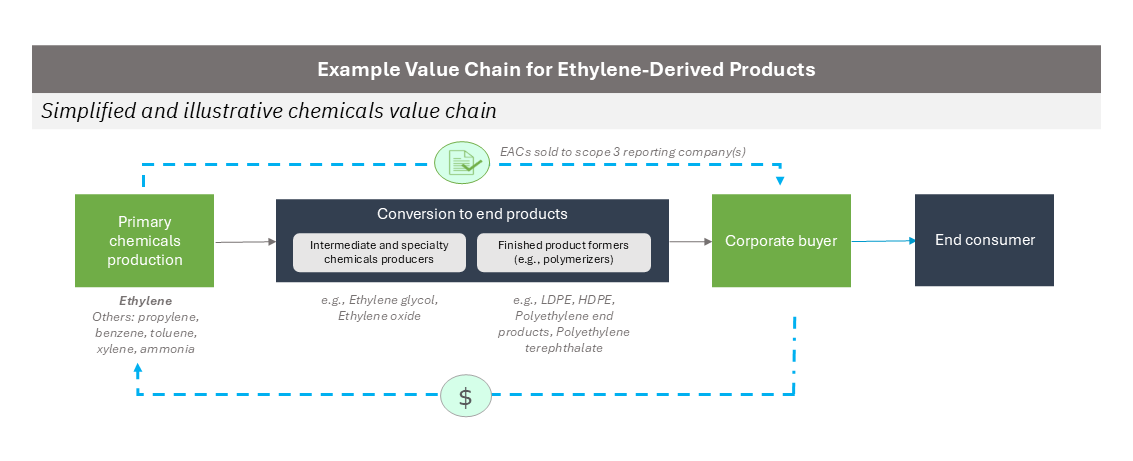

In cases where physical offtake of low-emission chemicals is constrained, book and claim systems provide a mechanism to aggregate larger demand volumes through the use of Environmental Attribute Certificates (EACs). Under this chain of custody approach, chemical producers generate an EAC for each unit of low-emission product, such as a ton of ethylene, that reflects the reduced emissions intensity associated with production. This certificate is then sold separately from the physical product, which continues through the value chain as a traditional commodity with a baseline emissions intensity. This separation enables chemical producers to receive revenue from EAC sales to cover the premium associated with low-emission production, providing the financial certainty needed to finance capital-intensive projects. At the same time, buyers gain verifiable, traceable progress toward climate commitments through certificates that are independently verified and tracked through a registry system.

The result is three benefits that can dramatically alter the viability of low-emissions production:

- 1: Value Chain Bridging: Perhaps the most significant impact of book and claim systems is the ability for interested parties to transact efficiently. By enabling standardized transactions between downstream brands willing to pay for value chain decarbonization and upstream producers that most heavily influence emissions, the challenge of aligning multiple intermediaries around price and volume in complex value chains can be avoided.

- 2: Geographic Aggregation: Book and claim provides an additional benefit, particularly in the early innings of the net-zero transition when access to low-emissions products remain limited. Creating an EAC distinct from the physical product means that a producer is no longer constrained to finding customers willing to pay a premium for a low-emissions product near its production plant. Instead, they can sell the physical product locally at commodity prices and cover the green premium by selling an EAC to any downstream user of the product, regardless of geography.

- 3: Product Aggregation: By focusing a book and claim system on high value chemicals, a third benefit can be realized. A traditional demand aggregation approach would need to find buyers procuring identical products. However, book and claim enables demand aggregation across any product that contains a particular molecule. For example, demand for low-emissions ethylene can be aggregated across apparel companies using polyester for textiles, pharmaceutical companies sourcing polyethylene for syringes, and personal care companies using multiple types of plastic for everyday household goods. By focusing on a common and consistent upstream input, substantially more demand can be aggregated and transacted in a single procurement.

Given the immense challenges associated with decarbonizing chemical production, leveraging novel mechanisms to catalyze investment in low-emissions production will be essential. Combining demand aggregation with book and claim in the form of a buyers alliance for EACs offers a unique opportunity to reduce risk for both buyers and suppliers, while driving real investment decisions.

GMA and RMI’s Low-Emissions Chemicals Initiative

An emerging initiative from GMA and RMI to procure low-emissions high value chemicals leverages these approaches to tackle emissions in the chemicals sector. Multiple downstream brands that use chemicals in their products have come together to procure environmental attributes for low-emissions ethylene, with plans to expand this approach to other molecules in the future. In the process, they will provide demand certainty for low-emissions projects while simultaneously finding a pathway to address upstream Scope 3 emissions that had previously been out of reach due to complex, multi-tiered value chains.

Prior efforts from GMA and RMI to pool advanced commitments for low-emissions products in heavy industry sectors have demonstrated how aggregated demand can generate confidence for suppliers and investors. Sectoral buyers alliances such as the Sustainable Aviation Buyers Alliance (SABA), managed by Environmental Defense Fund, GMA, and RMI, have shown how standardized frameworks and collective purchasing can accelerate the deployment of next-generation technologies. Launched in 2021, this effort has evolved from one-year advanced commitments to purchase bio-based sustainable aviation fuel (SAF) to a scaled marketplace and targeted 5+ year offtakes at scale for next generation fuels.

Without credible demand signals and effective mechanisms to translate that demand into firm offtake agreements, the transition will stall. GMA and RMI are working to bring these pieces together—aggregating demand and developing mechanisms to more efficiently enable offtake—to ensure that novel pathways to produce low-emission chemicals are developed. Together with active engagement from buyers and support from the broader ecosystem, these actions can provide the demand certainty needed to unlock investment and enable the chemical sector to accelerate its transition to a net-zero future.

If you are interested in learning more about the GMA-RMI low-emissions chemical procurement that was spotlighted in this article please reach out to chemicals@gmacenter.org.

Related News & Resources

04.29.26

Pilot Procurement Uses Collective Demand to Unlock Investment In Low-Emissions Chemicals

The Center for Green Market Activation and RMI launch first-of-its-kind request for proposals on behalf of corporates to scale low-emissions ethylene production.

The Center for Green Market Activation (GMA) and RMI today announced a first-of-its-kind pilot procurement for low-emissions chemicals, bringing together leading, early-adopter companies across industries, including technology, consumer goods, apparel, and food and beverage. Through a collective procurement, participating companies are sending a strong, coordinated market signal to address emissions embedded deep within the chemicals value chain, targeting approximately 3,000-10,000 mtCO2e per year in emissions reductions from low-emissions ethylene — a key building block used in many everyday plastic products ranging from packaging and medical supplies to construction materials and textiles.

GMA and RMI are now seeking responses from chemical producers capable of supplying verified low-emissions ethylene using eligible production pathways, with transparent emissions accounting and the ability to transact environmental attributes through a book and claim system. The procurement is designed to provide producers with an opportunity to monetize low-emissions production, helping to support the business case for scaling emerging and differentiated production pathways. The inaugural request for proposals (RFP) will also act as a proof of concept for future aggregated procurements of low-emissions chemical attributes.

“With this innovative pilot procurement for low-emissions ethylene, we’re excited to demonstrate the power of collective, corporate demand in the chemicals sector,” said Kim Carnahan, GMA CEO. “Through this pilot, we will have the opportunity to field test and refine our approach with an ambitious group of first movers and lay the groundwork for bigger buys and different molecules in future.”

Chemicals are crucial to modern society, yet little progress has been made toward decarbonizing chemical production. Historically, substantial barriers have constrained investment in low-emissions production pathways. These barriers include capital-intensive facilities, long asset lifetimes, thin operating margins, and complex supply chains that, together, have limited the ability of new technologies to secure the long-term demand needed to justify investment at scale.

As a result, companies that use chemicals in their products have struggled to address value chain emissions. While many are working to reduce or replace emissions-intensive inputs like ethylene, unavoidable residual demand remains, and companies are often several steps removed from primary production with limited visibility into the most emissions-intensive stages of their supply chains. Even where willingness to act exists, traditional procurement structures have made it difficult to translate that intent into meaningful emissions reductions.

This pilot procurement applies a novel approach to break that gridlock and enable action. By combining demand aggregation with a book and claim system, the procurement enables chemical producers to generate environmental attribute certificates (EACs) associated with low-emissions ethylene production and sell them separately from the physical product. This allows producers to receive revenue reflecting the lower emissions intensity of their production, while downstream companies gain a flexible, credible pathway to support low-emissions production and report associated claims in their climate disclosures.

“Voluntary demand has already proven to be a powerful catalyst for investment and innovation in sectors like renewable electricity and sustainable fuels,” said Thomas Koch Blank, managing director at RMI. “We’ve seen how established, forward-looking buyers can grow emerging markets, de-risk investment, and send strong demand signals that unlock capital at scale. We’re excited to explore how this pilot procurement for low-emissions ethylene can bring that same momentum to the chemicals sector.”

Versions of this approach have already been used successfully to jumpstart markets for low-emissions production in other hard to abate transport and heavy industry sectors, including the Sustainable Aviation Buyers Alliance, the Sustainable Steel Buyers Platform, and others. This pilot represents the first known application of a collective procurement and book and claim model to the chemicals sector.

The RFP is available for download here on the GMA website, and responses are due by July 3, 2026. For additional information about the procurement, please contact chemicals@gmacenter.org.

Media inquiries please contact:

Alison Greene, Communications Manager, GMA: alison.greene@gmacenter.org

About the Center for Green Market Activation:

The Center for Green Market Activation (GMA) is a US-based, globally focused non-profit. Through innovative procurement approaches and sector-specific buyers alliances, GMA catalyzes and scales the uptake of low-carbon goods and services within carbon-intensive industries including aviation, maritime, trucking, cement and concrete, and chemicals. With collective decades of experience in environmental markets and alternative fuels and materials, the GMA team works to standardize new, green markets and forges mutually beneficial partnerships between climate-focused companies, suppliers, and mission-aligned non-profit organizations to channel funding to critical climate technologies in pursuit of accelerated sectoral decarbonization. Learn more at gmacenter.org

About RMI:

Rocky Mountain Institute (RMI) is an independent, nonpartisan nonprofit founded in 1982 that transforms global energy systems through market-driven solutions to secure a prosperous, resilient, clean energy future for all. In collaboration with businesses, policymakers, funders, communities, and other partners, RMI drives investment to scale clean energy solutions, reduce energy waste, and boost access to affordable clean energy in ways that enhance security, strengthen the economy, and improve people’s livelihoods. RMI is active in over 50 countries.

Related News & Resources

04.22.26

GMA Newsletter Spring 2026 | Earth Day Edition

If you’d like to have these newsletters delivered directly to your inbox, subscribe to our mailing list through the form at the bottom of our homepage or email pr@gmacenter.org.

Happy Earth Day and happy birthday to us! Fun fact: GMA was incorporated on April 22, 2024, so we get to celebrate both. Not a bad alignment.

We’re so grateful to be doing this work, and our impact continues to grow. Now entering year three as an organization, we’re turning up the dial on implementation with major procurement milestones, new RFPs, fresh book and claim frameworks, and the eagerly awaited release of the AIM Platform’s Standard and Guidance to help unlock the next wave of decarbonization investment. Dive in below for the latest, and if you’re already thinking ahead to New York Climate Week, we’re gearing up for the third annual Green Markets Day on Tuesday, September 22nd — more to come soon.

Watch our latest explainer video, in which GMA’s Joan Gibbons explains why companies often can’t access low-carbon cement and concrete in their region and how book and claim can serve as an unlock and market accelerator.

Program Updates

Aviation

The Sustainable Aviation Buyers Alliance (SABA) has made significant advancements through both procurement and market infrastructure milestones. Infinium’s Project Atlas was selected as the winner of SABA’s next-generation SAF procurement, following a comprehensive, multi-stage review and due diligence process conducted on behalf of SABA’s corporate buyers. In parallel, the SAFc Registry surpassed 500,000 metric tons of CO₂e abated, reinforcing the strength of corporate demand for credible, scalable SAF solutions.

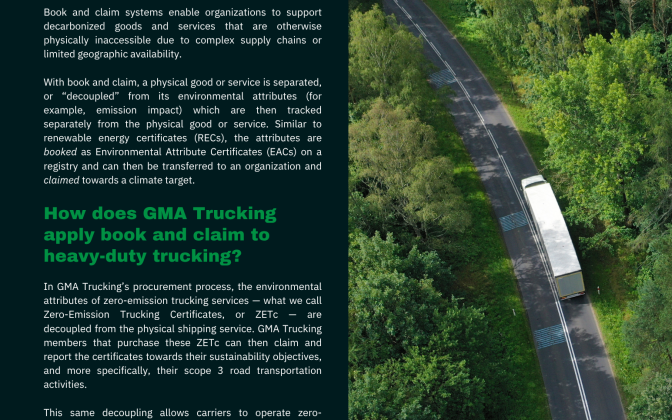

Trucking

The GMA Trucking team’s recently released whitepaper shares detailed findings from its pilot RFP, introduces the challenges GMA Trucking seeks to address, and explores the critical role of demand aggregation and book and claim. GMA Trucking also hosted a webinar on January 15th with speakers from the winning carrier, Nevoya, and corporate buyers Amazon and Etsy. The Trucking team is currently exploring procurement models for its second RFP and planning to integrate physical demand with book and claim for the first time. Get in touch if that sounds as exciting to you as it does to us!

Cement & Concrete

GMA’s cement and concrete program, run in partnership with RMI, finalized a sector-specific Book and Claim Framework in January, following extensive engagement across the value chain. The framework underpins SCoBA’s first RFP, launched in early April and targeting up to 85,000 tCO₂e per year of low emissions cement attributes. We encourage eligible cement producers to submit proposals via the GMA website through June 19, and look forward to seeing this process progress over the coming months.

Fertilizer

GMA Agriculture’s low-emission fertilizer program wrapped up its supplier outreach this spring, drawing responses from producers across a range of decarbonization technologies. The team is now meeting with buyers to define procurement criteria ahead of a formal RFP.

High-Value Chemicals

GMA Chemicals is advancing its pilot procurement for low-carbon ethylene (think plastics!) with an established buyer group and is set to launch its RFP in the coming days — paving the way for the first-ever book and claim offtakes for low-emission chemicals.

Maritime

Late last year, the Zero Emission Maritime Buyers Alliance (ZEMBA) announced that it will facilitate some of the first commercial e-fuel deployments in the maritime sector.

Members are supporting the deployment of both e-methanol and e-ammonia from 2027-2031. Contracting for these landmark deals is currently underway; freight buyers interested in lowering their Scope 3 maritime emissions should reach out through shipZEMBA.org to learn more!

The AIM Platform

The Advanced and Indirect Mitigation (AIM) Platform released V1 of its Standard and Guidance, providing companies with a clear, credible framework for investing in high-integrity emissions reductions across their value chains. The publication follows two pilot processes and public stakeholder consultation periods to ensure the Standard is actionable and applicable across sectors and technologies. A webinar marking the release took place April 21 – a recording is available here.

GMA in the News:

- SABA’s next-gen winner’s announcement was covered by the Sacramento Business Journal and picked up by the Financial Times among other outlets.

- GMA Trucking’s pilot procurement results were covered by Trellis, Commercial Carrier Journal, ACT News, American Journal of Transportation, and others.

- Andrew Alcorta was part of a Q&A article by QCI focused on how EACs can unlock investment in low-carbon fertilizer.

- Bloomberg News highlighted the Sustainable Concrete Buyers Alliance (SCoBA) as part of a January article on data center construction, and SCoBA also earned mentions in Financial Times and others, while the Cement and Concrete Book and Claim Framework was picked up by Concrete Products.

- The AIM Platform’s newly published Standard and Guidance was part of a Trellis article by Jim Giles.

#ICYMI:

- CEO Kim Carnahan spoke with Inder Singh for episode 6 of the Market Shapers Podcast, which will also be incorporated into a class at UC Berkeley on market shaping.

- GMA and partner programs were featured in the International Transport Forum’s recent publication: Claiming the Future: Can Book and Claim Support Low-Emission Transport?

- GMA’s Andrew Alcorta and Akhil Mithal joined RMI’s Patrick Malloy and Tessa Weiss in co-authoring “Cultivating a lower-carbon food supply chain: Unlocking Scope 3 progress through fertilizer emissions reduction.”

- Andre de Fontaine joined the ESG Decoded podcast to discuss how book and claim and demand aggregation can unlock value chain decarbonization.

- Recordings of recent webinars on GMA Trucking, Cement & Concrete, and the AIM Platform are all available here.

Upcoming Events

San Francisco Climate Week

April 18-26, 2026 | San Francisco, CA

GMA is part of multiple events and side-convenings. Reach out to connect!

Click here for more information.

ACT Expo

May 4-7, 2026 | Las Vegas, NV

GMA Trucking will have a number of representatives networking and available for in-person meetings.

Click here for more information.

Home Delivery World

May 20-21, 2026 | Nashville, TN

Clayton Gerber is an invited speaker, including on the keynote panel “Delivering net zero, meeting the sustainability challenge in logistics”

Click here for more information.

Decarb Connect Europe

June 2-3, 2026 | Hamburg, Germany

GMA is an official media partner of Decarb Connect Europe, where Laura Hutchinson is an invited speaker. The conference brings together senior industrials, investors, project developers and buyers who are actively working on capital allocation and deployment decisions in 2026. To receive a special 25% discount on registration, please use the code GMA-25.

Learn more and register here.

Trellis Impact 2026

June 23-25, 2026 | San Francisco, CA

GMA will be a part of multiple workshops and panels, including “Aggregated and Activated: How Buyers Alliances are Accelerating Green Market Transformation” as well as a session focused on environmental attribute certificates.

Learn more and register here.

London Climate Week

June 21-29, 2026 | London, UK

GMA representatives will be circulating at events throughout the week, more details to come.

New York Climate Week

September 21-28 | New York City

GMA will host our third annual Green Markets Day on Tuesday, September 22nd – email pr@gmacenter.org to be added to event-related communications.

Related News & Resources

04.08.26

Buyers Unite to Accelerate the Market for Low-Carbon Cement

The Sustainable Concrete Buyers Alliance launches a first-of-its-kind procurement, calling for proposals to supply low-emissions cement to meet corporate demand.

WASHINGTON, D.C. – Apr. 8, 2026

The Sustainable Concrete Buyers Alliance (SCoBA), a joint initiative of the Center for Green Market Activation and RMI, today launched a request for proposals (RFP) to secure multi-year offtake agreements supporting up to 250,000 tons of low-carbon cement production annually, beginning as early as 2027. It marks the first phase of a procurement designed to overcome persistent barriers that have slowed decarbonization across the construction sector.

Cement and concrete are vital to the built environment, from housing and commercial buildings to data centers and transportation networks, and global demand for cement is expected to increase to 6.2 billion tons by 2050. Cement accounts for most of the sector’s global emissions, yet emissions-reducing technologies often face geographic and cost barriers to scale, limiting access for many organizations. Through this RFP, SCoBA will enable its climate-ambitious member companies to abate up to 85,000 metric tons of CO2e emissions per year, subject to final commercial details.

The procurement will target offtake from innovative cement producers while sending a catalytic signal to the market. The inaugural RFP is open globally to products meeting the Global Cement and Concrete Association’s low-carbon cement definition of Band B or better, roughly equivalent to at least a 67% emissions reduction compared with today’s industry reference level. SCoBA aims through this procurement to pool buyer demand, secure high-integrity supply, and enable innovative, low-carbon production methods to scale.

“Decarbonizing cement is essential to tackling emissions in the built environment, but progress has been constrained by fragmented demand and limited access to low-carbon solutions,” said Bryan Fisher, managing director of RMI’s industries program. “We’re excited to be entering the next phase of our cement and concrete demand initiative with GMA, connecting leading companies with cutting-edge producers to secure the long-term offtake agreements project developers need to confidently pursue decarbonization projects in this critical industrial sector.”

SCoBA launched in 2025 as a program of the Center for Green Market Activation (GMA) and RMI to pool demand from end-use customers and channel investment through bankable agreements, giving low-carbon cement and concrete producers the confidence to scale. Since its launch, SCoBA has engaged the market to design a procurement that is ambitious, globally focused, and capable of accelerating new production of truly sustainable low-carbon cement.

“Our outreach to the market confirms a growing pipeline of low-emissions cement solutions seeking credible demand,” said Kim Carnahan, CEO at GMA. “SCoBA’s innovative procurement brings that demand together, sending a signal individual buyers cannot achieve alone. This is about turning climate ambition into real market movement.”

The procurement will use a book and claim framework developed and recently launched by GMA and RMI, allowing companies to support low-carbon production even when the physical material cannot be delivered directly to their projects. Buyers purchase verified environmental attribute certificates representing the emissions associated with low-carbon cement or concrete, which they can retire and count toward Scope 3 goals, while the material itself is deployed where it is most practical. This model helps overcome geographic and logistical constraints that have historically limited access to lower-emission building materials and provides producers with streamlined access to committed buyers.

SCoBA’s procurement builds on proven demand aggregation models pioneered by the Sustainable Aviation Buyers Alliance and expanded to additional transport sectors such as maritime (Zero Emission Maritime Buyers Alliance) and heavy-duty trucking (GMA Trucking). This program represents a second application of that approach to the built environment; the first being the Sustainable Steel Buyers Platform.

Low-carbon cement suppliers are invited to download the RFP and submit proposals by June 19, 2026. Interested parties can also register for a webinar, scheduled for April 15 at 11AM ET. Companies with Scope 3 cement and concrete emissions who are interested in purchasing through this pilot procurement can explore SCoBA membership by emailing info@buildscoba.org.

Media inquiries please contact:

Amy Yanow Fairbanks, Strategic Communications Manager, RMI: media@rmi.org

Alison Greene, Communications Manager, GMA: pr@gmacenter.org

About the Center for Green Market Activation:

The Center for Green Market Activation (GMA) is a US-based, globally focused non-profit. Through innovative procurement approaches and collaborative alliances, GMA catalyzes and scales the uptake of low-carbon goods and services within carbon-intensive industries such as aviation, maritime, trucking, cement and concrete, and chemicals. With collective decades of experience in environmental markets and alternative fuels and materials, the GMA team works to standardize new, green markets and forges mutually beneficial partnerships between climate-focused companies, suppliers, and mission-aligned non-profit organizations to channel funding to critical climate technologies in pursuit of accelerated sectoral decarbonization. Learn more at gmacenter.org

About RMI:

Rocky Mountain Institute (RMI) is an independent, nonpartisan nonprofit founded in 1982 that transforms global energy systems through market-driven solutions to secure a prosperous, resilient, clean energy future for all. In collaboration with businesses, policymakers, funders, communities, and other partners, RMI drives investment to scale clean energy solutions, reduce energy waste, and boost access to affordable clean energy in ways that enhance security, strengthen the economy, and improve people’s livelihoods. RMI is active in over 50 countries.

Related News & Resources

01.28.26

Article | Cultivating a lower-carbon food supply chain: Unlocking Scope 3 progress through fertilizer emissions reduction

Authors: Andrew Alcorta and Akhil Mithal (Center for Green Market Activation), Patrick Molloy and Tessa Weiss (RMI)

Agriculture accounts for roughly one-quarter of global greenhouse gas emissions, yet its pathway to achieving net zero defies simple solutions. A wholly climate-friendly food system will require multiple interventions happening in parallel — from regenerative agriculture practices and precision fertilizer techniques to fundamental changes in how we produce the products that help us grow, feed, and support the food we eat. Many of these interventions require behavioral changes across millions of farms that will take time to scale, underscoring the importance of acting decisively where impact can be achieved today. Fertilizer production represents one such opportunity where companies can drive verifiable emissions reductions in the near term.

Nitrogen fertilizers support crops that feed roughly half the world’s population, making them foundational to global food security. The scale of this dependence is stark — without synthetic nitrogen inputs, it is projected that global cereal production would decline by approximately half. While regenerative agriculture practices offer important soil health benefits, relying solely on biological nitrogen fixation would likely require surrendering even more land to crops to maintain current production levels. And the challenge is intensifying: as the global population approaches 10 billion by 2050, fertilizer demand is projected to increase by roughly 35 percent, increasing pressure for continued fossil-linked fertilizer production.

Yet nitrogen fertilizers carry an outsized climate footprint: their production, distribution, and use generate an estimated 1.31 gigatons of CO₂-equivalent emissions annually – the same emissions as consuming 3 billion barrels of oil. Approximately 40 percent of those emissions originate from fertilizer production itself.

Solutions to produce fertilizer with far fewer emissions already exist – renewable-powered electrolysis can eliminate these production emissions entirely – but they cost more than fossil-intensive processes today. Scaling these solutions requires long-term financial commitments that fertilizer producers’ direct customers – input producers and farmers operating on thin margins – are unable to provide. Food and beverage companies face a distinct but related challenge: they need to reduce supply chain emissions, also known as Scope 3 emissions, from the agricultural products they purchase – driven by investor pressure, regulators and sustainability commitments – but lack a mechanism to effectively do so.

The Center for Green Market Activation (GMA) and RMI are launching a pilot book and claim procurement to bridge this gap. In this system, food and beverage companies can financially support low-emission fertilizer projects through the purchase of Environmental Attribute Certificates (EACs) and claim verified emissions reductions toward Scope 3 targets — without requiring physical delivery of low-carbon product through their existing supply chains. Low-carbon fertilizer producers receive revenue certainty to cover green premiums, buyers gain measurable progress on climate commitments, and farmers continue purchasing fertilizer through conventional channels without having to pay more or disrupt their operations.

Scaling technologies to produce low-emission fertilizer

A suite of low-emission fertilizer solutions exists today that can deeply decarbonize production while offering broader benefits like increased supply chain resiliency. Projects like First Ammonia’s in Texas and startups such as NitroVolt, Atlas Agro and TalusAg are pioneering scalable green ammonia production using renewable energy and novel synthesis processes. These technologies can significantly reduce production emissions, increase farmer autonomy over crop nutrition through localized production, and have the potential to reduce input price risk by decoupling fertilizer costs from volatile fossil fuel markets.

However, scaling these solutions faces critical structural barriers. Fertilizer producers need to know they have long-term committed buyers to finance capital-intensive low-emissions projects — but farmers, who typically purchase fertilizer seasonally and operate on thin margins, are unlikely to absorb cost premiums. Further downstream, food and beverage corporations possess both the relative willingness to pay and the creditworthiness needed to support project financing. While low-emission fertilizer currently costs more to produce, the impact on food companies is minimal: premiums would translate to only 1-2% increases in packaged goods prices, far smaller than routine volatility from fuel or commodity markets. Critically, with at-scale deployment, the production cost of green ammonia can decline over time due to learning effects and scale efficiencies.

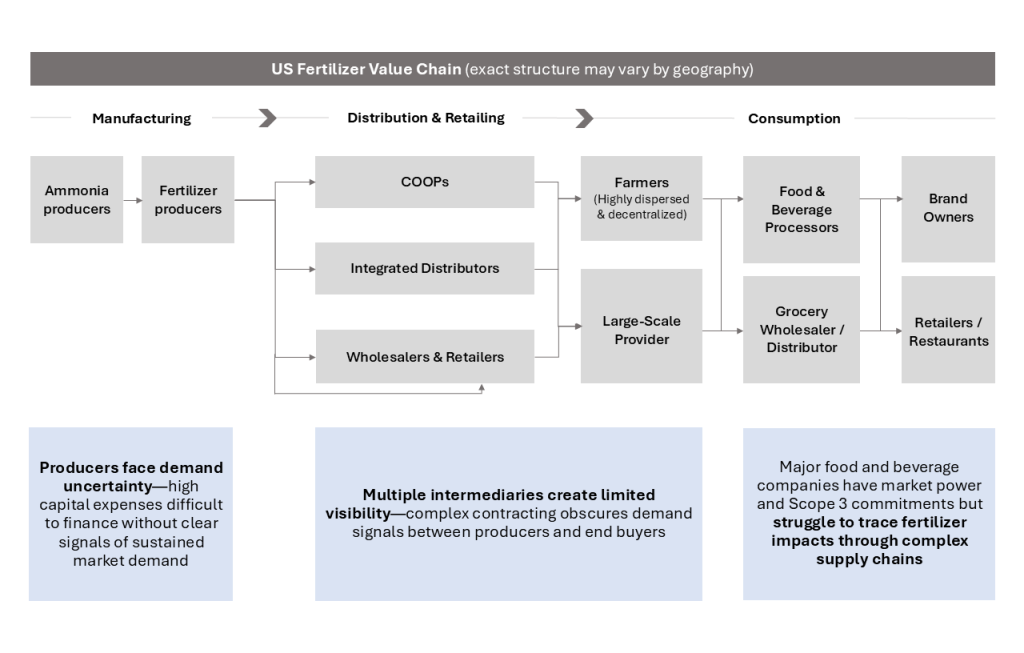

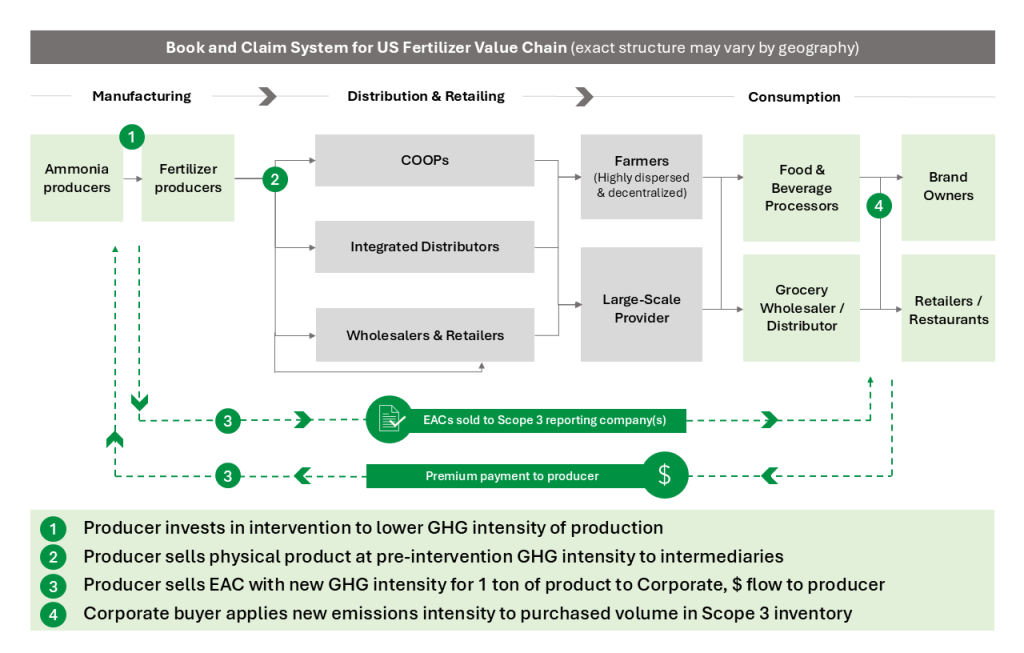

The challenge is that these corporate buyers sit 5-6 steps in the supply chain away from fertilizer manufacturers and have no established mechanism to directly procure or contract for low-emissions fertilizer (Exhibit 1). This long and often fragmented value chain prevents fertilizer producers from monetizing low-emissions production because they lack a relationship with the parties that most value decarbonization.

Exhibit 1: US Fertilizer Value Chain

More than 900 companies across food, beverage, consumer packaged goods (CPG), and agriculture sectors have validated near-term Science-Based Targets under SBTi. Under the GHG Protocol’s Agricultural Guidance, they must account for full value chain fertilizer emissions in their Scope 3 inventories, including fertilizer emissions that can represent a substantial portion of their total GHG footprint. Yet these companies effectively have no way to manage these emissions today: they lack direct relationships with fertilizer producers, creating a gap between sustainability commitments and the operational levers needed to achieve them.

Bridging a Value Chain Gap through Environmental Attribute Certificates (EACs)

Book and claim systems solve this challenge by decoupling environmental attributes from physical product flow. Under this framework, fertilizer producers generate Environmental Attribute Certificates (EACs) for each unit of low-emission production, which are then sold separately from the physical fertilizer itself (Exhibit 2). Corporate buyers purchase these certificates to demonstrate verified emissions reductions in their Scope 3 inventories, creating a direct financial channel between producers and corporate buyers — regardless of where the physical fertilizer ultimately flows through agricultural supply chains. This structure enables revenue to reach decarbonization projects without requiring companies to engage in complex coordination that alters how farmers source inputs or require that physical molecules are traced all the way through complex value chains.

Exhibit 2: Book and Claim System for US Fertilizer Value Chain

The mechanism aligns incentives across the value chain. Fertilizer producers receive revenue from EAC sales to cover the premium associated with low-emission production, providing the financial certainty needed to finance capital-intensive projects. Buyers gain verifiable, traceable progress on climate commitments through certificates that are independently verified and tracked through registry systems. The physical low-emissions fertilizer enters conventional distribution channels where farmers purchase it at commodity prices, avoiding the need for farmers themselves to spend time sourcing or pay premiums for low-emissions inputs.

GMA and RMI’s Low-Emissions Fertilizer Initiative

GMA and RMI are launching a pilot book and claim procurement to enable fertilizer production decarbonization at scale. By aggregating demand from food and beverage companies with Scope 3 commitments, this initiative will create the collective purchasing power needed to de-risk producer investments and accelerate decarbonization technology deployment. Collaborative buyers alliances can help solve challenges in financing of first-of-a-kind projects by pooling demand across multiple companies, transforming fragmented demand pools into concentrated market signals. This collective approach shares transaction costs, aligns common standards, and delivers the forward contracts that make projects bankable, turning corporate sustainability commitments into impact delivered by real-world investments.

This approach builds on proven models that catalyze investment in new technologies by decoupling emissions attributes from commodity products. Renewable Energy Certificates (RECs) utilized this framework in electricity markets, and similar frameworks are being used for aviation, steel, cement, trucking, maritime fuel, and plastics, accelerating deployment of decarbonization technologies and catalyzing private investment across hard-to-abate sectors.

Across these sectors, success has depended on rigorous market infrastructure. As neutral technical experts, RMI and GMA establish frameworks that balance environmental credibility with commercial practicality — developing clear sustainability criteria for qualifying projects, robust verification protocols, and transparent registry systems that prevent double-counting and ensure corporate investments translate into genuine emissions reductions. By adapting this model to fertilizer, we aim to unlock the financing needed to scale green ammonia and other low-emissions production pathways, addressing one of agriculture’s most entrenched emission sources and giving food and beverage companies a credible path to meet their Scope 3 targets.

Ready to join? If your company has a Scope 3 target that includes fertilizer emissions in your supply chain, this initiative offers an opportunity to achieve your goals and catalyze meaningful agricultural decarbonization. To learn more about participating in the pilot procurement, please contact us at chemicals@gmacenter.org.

Related News & Resources

12.16.25

GMA Newsletter | A Look Back at 2025

A look back at 2025:

From collective ambition to market transformation

With 2025 soon to be in the rear view, we find ourselves at the midpoint of a pivotal decade for climate action. While the political forecast remains, shall we say, variable, and momentum on climate action has been tested, the organizations we partner with every day continue to champion ambitious voluntary decarbonization commitments.

This year’s progress proves what is possible when motivation is matched with action and grit. (Take a look at our year-end video, above, for some of the high points!) None of it would be possible without the active engagement of hundreds of stakeholders with our programs – thank you for being such a central part of this work.

Before we officially wrap up the year we wanted to highlight milestone developments across two GMA program areas: zero emission trucking and standards and guidance.

A year after launching GMA Trucking’s pilot RFP, we are on the cusp of finalizing contracts for our first procurement for zero emission trucking service attributes. This pilot has shown what’s possible when companies join forces, with demand aggregation and book and claim proving to be powerful levers for getting more zero emission trucks on the road. This effort now sets the stage for even larger procurements starting in 2026.

Among the standout achievements from this first-of-a-kind effort:

- It will result in the largest known deployment of heavy-duty EVs in Texas, and

- It channels catalytic investment to a zero-emissions technology start-up.

(If you missed our announcement of Nevoya as the winning carrier during New York Climate Week, see these video highlights.)

The procurement structure leverages innovative commercial terms, is designed to maximize truck utilization, and helps overcome current barriers to EV trucking. We’ll share more early next year when we announce the full RFP results. In the meantime, mark your calendars for our webinar on January 15 – your backstage pass to lessons learned and what’s coming next.

Companies have been clear – the GHG accounting and target setting standards must evolve to support credible, innovative scope 3 decarbonization. This year, the AIM Platform continued to lead the development of robust methods for companies to take action deep in their value chain and transparently report those efforts.

2025 also saw both the Science Based Targets Initiative (SBTi) and GHG Protocol (GHGP) recognize the importance of value chain mitigation. We applaud their commitment and continue working closely with both to ensure alignment and interoperability across frameworks.

Over 2025, the AIM Platform:

- Conducted pilot tests and public consultation on the AIM Platform Association Test and the Intervention Quality, Accounting and Reporting (QAR) Standard and Guidance,

- Released a draft Electricity Annex for stakeholder consultation, and

- Engaged over 40 leading organizations whose real-world testing is directly informing the tools to come.

This collective input will shape the complete AIM Platform Standard and Guidance we expect to publish in Q1 2026. Stay tuned – 2026 is going to be another big year for game-changing developments in the standards space.

In brief:

- Jim Giles featured multiple GMA programs in a recent Trellis article on the growing use of environmental attribute certificates.

- If you attended COP30, the SABA COP30 SAF platform remains open for purchases through the end of this year. The first several hundred purchases will have double the impact through a matching sponsorship courtesy of Airbus.

- Trellis highlighted the AIM Platform QAR pilot, which was also the subject of a webinar held earlier this fall. You can access a recording here.

- #ICYMI, a session-by-session video library from Green Markets Day 2025 can be accessed from our website.

With gratitude:

To our partners at Aspen Institute, C2ES, EDF, Gold Standard, RMI, and Smart Freight Centre – we deeply value the opportunity to work alongside you. We are in this together for as long as the need exists, and look to the new year with optimism, excitement, and resolve. And to everyone at GMA – thank you for the irreplaceable skill, commitment, and spirit of collaboration you bring to our work together. We are so fortunate to have each of you as part of this dream team.

Best wishes for a safe, healthy, and happy holiday season!

See you in 2026!

Related News & Resources

12.08.25

As Seen in Trellis: A wonky accounting device is becoming an essential part of climate strategies

In a Trellis article published December 4, 2025, Editor-at-Large Jim Giles takes a closer look at environmental attribute certificates and how they are helping drive new and catalytic investment to decarbonized fuels, technologies and services. The article kicks off with a nod to the growing awareness of and implementation of programs using EACs, followed by a quote from GMA CEO Kim Carnahan:

– – – – – – – – – – – – – –

“This may have been the year when a somewhat wonky component of sustainability strategy — the environmental attribute certificate (EAC) — went mainstream. The past 12 months have seen certificates for low-emission products minted in multiple sectors, including cement, iron and carbon capture. In parallel, standard setters are close to giving companies greater leeway to use certificates in carbon accounting and target setting.

‘It definitely feels like this year something really clicked across the board — with buyers and suppliers, but also the standard setters seem to be getting it, the environmental NGOs, even governments,’ said Kim Carnahan, CEO of the nonprofit Center for Green Market Activation (GMA).'”

– – – – – – – – – – – – – –

The article continues with an exploration of various sectors where EACs are working to overcome market barriers, highlighting individual projects helping decarbonize data centers as well as buyers alliances that aggregate demand for low and zero emission solutions from groups of climate-leading companies, allowing them to send a stronger signal to the market and support growth in supply. These include programs that GMA co-manages alongside our NGO partners, including the Sustainable Aviation Buyers Alliance (SABA), Sustainable Concrete Buyers Alliance (SCoBA), zero-emission trucking and low-carbon chemicals.

Click here for the complete article.

Related News & Resources

11.13.25

Perspectives on SBTi’s Second Draft Corporate Net Zero Standard V2 from GMA CEO Kim Carnahan

Following the release of the second draft of the corporate net-zero standard V2 from SBTi on November 6th, 2025, GMA CEO Kim Carnahan shared her insights on what this update means for sector-level decarbonization efforts and programs that utilize book and claim, and where opportunities remain to refine the final draft to make it most useful and effective. GMA encourages stakeholders to engage with the public consultation period that ends December 8, 2025.

Kim’s original LinkedIn post is copied here, below.

“ICYMI: the next version of the DRAFT V2 Science Based Targets initiative Corporate Net Zero Standard is out.

It’s clearer, (somewhat) simpler, and takes many steps in the right direction.

It includes even more clarity (compared to the last draft) that indirect mitigation will count towards climate targets.

The First Public Consultation Feedback Report, also released today, shows why: ~80% of respondents supported counting indirect mitigation toward target achievement. Mandate sent.

I specifically like several adjustments they made to the indirect mitigation concept – now called “sector level actions.” The Advanced and Indirect Mitigation (AIM) Platform (www.aimplatform.org) supports this theory of change: even if a company lacks traceability or direct access to solutions, they still need to work to decarbonize the sectors that form the building blocks of their business.

Unfortunately, a few BIG holes remain in this otherwise gold star product.

Hole #1

– The draft appears to say that indirect mitigation can count towards some but not all scope 3 target types. I am perplexed as to why the clear mandate received would apply to some but not all target types.

– I get the current situation is complex with the overlapping GHG Protocol revision process. But one thing is not complex: Companies need the strongest and loudest signal possible to invest in critical decarb technologies now – and it is SBTi’s job to give that signal.

– GHG Protocol is policy agnostic and can provide the tools to meet any target. In fact, it has already convened a technical working group (I’m a proud member) to develop them.

Hole #2

Where is project-based accounting for indirect mitigation? I’m a huge proponent of product based, attributionally accounted EACs but some (very important) work requires project-based accounting. There needs to be a clear place for it in target achievement, or it simply won’t get done.

Hole #3

What about companies who already have V1 targets? I realize this standard will apply to future targets but we need a cover page (or similar) that clearly states that indirect mitigation will count, in all the same ways, to V1 targets.

And finally, with the overall complexity of the target setting approach outlined in this draft: I understand what SBTi is trying to engineer with this approach. I’m worried that logic will not equal effectiveness in this case, however. Companies need to be able to communicate these targets, clearly and succinctly – internally and externally. SBTi and all of us who support them will be more successful if companies can distill all the targets and sub-targets into the language we speak now – emission reductions.

All in all, huge progress. I very much believe we will get there in the final draft.”

Related News & Resources

10.29.25

Green Markets Day 2025 – Session Recordings Now Available

Green Markets Day 2025, held on September 23 during New York Climate Week, highlighted groundbreaking efforts and innovative approaches turning climate ambition into real-world action.

The Center for Green Market Activation, in partnership with Lowercarbon Capital and in collaboration with RMI and Smart Freight Centre, brought together suppliers, investors, standard-setters, and policy leaders for an unforgettable afternoon of candid debate, bold advances, and practical insights on scaling solutions in the toughest sectors to decarbonize – no matter which way the political winds blow.

Video recordings and transcripts are available at the links below by clicking on each session title.

Session Recordings

Welcome and State of the Market

Kim Carnahan, CEO, Center for Green Market Activation (GMA)

Trucking RFP Winners Announcement followed by Panel – Big Bet: Unlocking the Future of Trucking

Andre de Fontaine, Managing Director, GMA (moderator)

Christoph Wolff, CEO, Smart Freight Centre

Melissa Bauer, ESG and Sustainability Strategy Lead, eBay

Sami Khan, Co-Founder and CEO, Nevoya

SABA Spotlight: COP30 Campaign Announcement

Andrew Chen, Principal, RMI

Climate Intelligence Spotlight: RMI’s Climate Intelligence ‘Catalytic Procurement’ Report

Josh Henretig, Managing Director, RMI

Fireside Chat: Can Advance Market Commitments Jumpstart Climate’s Hardest Sectors?

David Roberts, Writer and Owner, Volts Podcast

Clay Dumas, General Partner, Lowercarbon Capital

Panel – Reaching Scale, Attracting Capital

Paul Bodnar, Director of Sustainable Finance, Industry, and Diplomacy, Bezos Earth Fund (moderator)

Brandon Middaugh, GM/Partner, Sustainability Markets and Climate Innovation Fund, Microsoft

Laura Helman, Senior Vice President, Brookfield

Rama Variankaval, Global Head of Corporate Advisory and Sustainable Solutions, JPMC

Jigar Shah, Co-Managing Partner, Multiplier

Campaign Spotlight: Mission Possible Partnership’s Build Clean Now Campaign

Michel Frédeau, Senior Fellow, Mission Possible Partnership

Panel – Concrete Steps, Steel Resolve, and Clean Chemistry: Heavy Industry’s Next Moves

Bryan Fisher, Managing Director, RMI (moderator)

Chris Atkins, Director, Worldwide Operations Sustainability, Amazon

Leah Ellis, CEO and Co-Founder, Sublime

Johan Mandaric Reunanen, Climate Impact Lead, Stegra

Hans Olav Raen, CEO, Yara Clean Ammonia

Panel – Founders at the Frontier: Startup CEOs Talk Scaling Climate Tech

Lauren Faber O’Connor, Partner, Lowercarbon Capital (moderator)

Gregory Constantine, CEO and Founder, AirCo

Sarah Lamaison, Co-Founder and CEO, Dioxycle

Sandeep Nijhawan, CEO, Electra

Hiro Iwanaga, CEO, TalusAg

Related News & Resources